Navigating Medicare: What You Need to Know About Out-of-Network Coverage

What You Need to Know About Out-of-Network Coverage

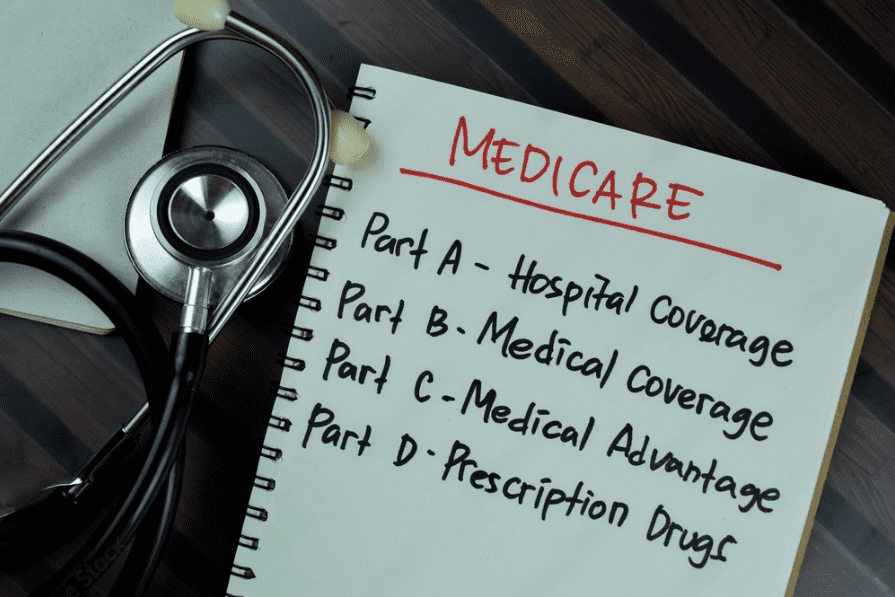

The Different Types of Medicare and Coverage Types

Firstly, let’s gain a little more understanding of Medicare by breaking down the various types and what they cover.

Original Medicare (Parts A and B)

Medicare Parts A and B, or Original Medicare, is the most well-known form of Medicare. Part A is known as hospital insurance, and part B is medical insurance. In other words, this Medicare will cover general doctor or hospital visits.

Medicare Advantage (Part C)

Medicare Part C is also known as the Medicare Advantage Plan. This is a plan approved by Medicare that is offered through a private insurance company. It will include both Part A and Part B, as well as Part D in many cases, which is detailed below.

Medicare Part D

Medicare Part D is prescription drug coverage.

This can be bundled into Original Medicare or Advantage to ensure your prescriptions are covered as part of your care.

In-Network vs Out-of-Network

Now, let’s take a look at what it means to be in-network or out-of-network. A network is essentially a group of providers and healthcare facilities that have partnered with Medicare or other health plans to provide care at an agreed price. This allows those under that insurance coverage to receive more affordable care without paying as much out of pocket.

So, when a physician or facility is in-network, it means they have contracted with that insurance company to provide services at a Medicare-approved amount. When a doctor or facility is out-of-network, they have not agreed to a contract or opted out, as it’s commonly called. Instances of this can potentially lead to no coverage or a significantly less covered service, which can mean more money out of pocket.

How Medicare Handles Out-of-Network Coverage

The fortunate thing about Medicare is that it has a network that spans all 50 states. Meaning you can find a doctor or facility that will accept it no matter where you are, in most cases that is. A vast majority of service providers do accept Medicare as a form of payment, but there are still some who don’t. However, two types of out-of-network coverage may be encountered with a Medicare plan, which are:

– Non-Participating Providers: Some providers may not agree to be in the Medicare network, but they may accept it in some cases. These are known as “non-participating” providers. Medicare may cover these services, but it could be on a reimbursement basis. Meaning you may have to pay the full cost upfront, and the provider should submit a claim to Medicare. If they don’t or refuse, you can submit one yourself.

– Opted-Out Providers: Providers who don’t want to accept Medicare as payment at all can opt-out, as mentioned above. In these cases, Medicare won’t cover any services from these providers except for emergencies.

It is important to remember that there is always a potential risk of higher out-of-pocket costs for out-of-network providers.

Additional Factors That Affect Out-of-Network Coverage

There can also be other factors that affect out-of-network coverage, such as differences between Original Medicare and Medicare Advantage. For instance, while Original Medicare can be used at any facility in the states that accepts it, Medicare Advantage may be restricted to specific service areas.

There can also be varying out-of-pocket costs between the two. For instance, you must pay a premium for Part B with either type of Medicare, but Medicare Advantage also includes a plan premium. Paying this plan premium could also mean fluctuating out-of-pocket costs for certain services. The benefit is that Medicare Advantage plans may offer service coverage that Traditional Medicare doesn’t, such as vision, dental, and hearing. To learn more about the differences between Original Medicare and Medicare Advantage, check out Medicare.gov’s comparison here.

Additionally, there are other options to help cover various costs that may arise, such as Medicare Supplement Insurance (Medigap). This extra insurance can be purchased from a private insurance company to help cover your out-of-pocket costs with Original Medicare.

While each plan has its pros and cons, it really comes down to the type of coverage you will need and where you will need it.

Navigating Out-of-Network Coverage

With all of the potential extra costs from out-of-network services, it is critical for you to be informed. Part of this is researching the providers within your Medicare plans network, as well as coverage options for their services. This also includes planning out what type of services you will generally need and whether you will be in other service areas where you need coverage.

Understand Referrals and Authorization Requirements

In the world of insurance, there are also referrals and authorizations. Let’s take a little more detailed look into what these mean.

– Referral: A referral is when your primary care physician refers you to see another provider, such as a specialist in a particular sector of healthcare. (Cardiologist, Gastroenterologist, etc.)

– Authorization: The authorization, or prior authorization, is approval from your healthcare plan to receive a service and have it covered.

With Original Medicare, you may get a referral to other providers, but it is rare for it to need prior authorization, provided they accept Medicare. However, with some of the Medicare options from private insurance companies, you will need to find out their particular policy on this. Otherwise, you may receive service that isn’t covered because it wasn’t correctly authorized.

Additional Resources to Learn About Medicare

The more you know about your particular Medicare health plan and its coverage, the better. It can help you locate the right providers for your coverage and avoid or reduce significant out-of-pocket costs. Some other resources are included below to learn more about the various plans.

– Comparison Between Original Medicare and Medicare Advantage Plans

– Medicare Supplement Insurance (Medigap)

– Providers Accepting Medicare

– What Isn’t Covered by Original Medicare

If you are still uncertain about what type of plan may be best for you, it is a good idea to consult with a Medicare counselor. They can offer personalized guidance to help you choose the right option for your Medicare coverage.

The Wrap on Medicare Out-of-Network Coverage

Navigating Medicare coverage can seem like a lot, but using the above information, you can start sorting out the right plan for you. Remember to research what providers are included in your network, what your plan covers, and any additional coverage you may need for your health. We know it can seem confusing to sort through all of this information, but we are always here to help you navigate coverage if needed!

We’re here to help! Call us today.