MEDICARE BASICS

First, you should understand that Medicare was created to give people in the aging population the ability to find affordable and adequate healthcare insurance.

The program gives health care coverage for every U.S. citizen who is over age 65. (It also provides insurance for people younger than 65 that receive Social Security Disability Insurance or those that have end-stage renal disease.)

Given the age and medical conditions of citizens in these groups, the private insurance sector did not want to insure them. It wasn’t a good investment for traditional insurance carriers and so they were being refused coverage.

In order to fix this serious social issue and make health insurance available to all people regardless of their age or disability, the United States federal government created the Medicare program. It serves as a kind of social safety net.

Because of this, the Medicare program is funded in part by Social Security and the Medicare payroll taxes which people pay on their income throughout your career, and it is also supplemented with money from the federal budget. Additionally, everyone who enrolls in Medicare must pay a premium to use the program.

THE MEDICARE PROGRAM

Medicare is organized into Parts, specifically Parts A, B, C, and D.

When you sign up for Medicare, you have to choose which Parts you want and your premium will vary depending on the particular Parts you opt for.

Each Part covers specific medical costs.

In this article, we will discuss each part so you can understand what coverages each one provides and what things they do no cover.

First, it’s important to realize that there are two main categories of Medicare coverage: Original Medicare and Medicare Advantage.

Original Medicare is a traditional fee-for-service program offered directly through the federal government. Medicare Parts A and B make up Original Medicare. These Parts cover hospital care and outpatient care. (We will get more specific in a moment.)

For now, understand that you do not have to pay a premium for Part A, but you do have to pay one for Part B. You cannot enroll in Part A alone. If you enroll in Part A, you must also enroll in Part B and pay the premium.

Medicare Advantage is an insurance policy provided by a private health insurance company which contracts with the federal government to provide healthcare coverage. Medicare Part C makes up Medicare Advantage.

Part C covers hospital care and outpatient care and we will talk more about this later. You must pay a premium for Part C. Most Medicare Advantage plans also include Part D coverage, which covers prescription drugs.

When you enroll in Medicare you will choose one of these two ways—either Original Medicare or Medicare Advantage—in order to receive your Medicare benefits.

WHAT IS COVERED AND NOT COVERED UNDER

ORIGINAL MEDICARE (PARTS A AND B)?

PART A COVERAGE

As we said earlier, Part A is the part of Medicare that covers hospitalization and inpatient care, which means it pays for any hospital costs related to hospital care or any medical care in a received in a skilled nursing facility or nursing home. It also covers the costs of hospice care and home health services.

All the care you receive as an inpatient care is covered under Part A, including inpatient medical supplies and prescription drugs you receive while you an inpatient. Also, if you happen to be homebound, Part A will cover physical and occupational therapy. Part A also covers expenses related to doctor visits, medication, and grief counseling for terminally ill patients.

THINGS PART A DOESN’T COVER

Medicare Part A will not cover every hospital procedure you may need. You can check the procedure or test you need on the Medicare website to make sure it is covered before you have it done. Click here to check.

If you need certain care that Medicare doesn’t cover, you will have to pay for those procedures or services out-of-pocket unless you have supplemental insurance.

Some things that are not covered under Medicare Parts A and B are:

- Long-term care (also called custodial care)

- Most dental care

- Hearing aids and exams for fitting them

- Eye exams related to prescribing glasses

- Dentures

- Cosmetic surgery

- Acupuncture

- Routine foot care

Whenever a patient needs a procedure which is not covered, providers are required to inform patients of this and have them sign a release prior to receiving treatment. This allows patients to opt to pay for the service out-of-pocket or refuse the care.

Remember that Medicare also doesn’t cover your deductible, co-insurance, or copayments. See the chart below to understand these costs better.

WHAT IS A DEDUCTIBLE?

- A deductible is the amount you must pay out-of-pocket for health coverage BEFORE your insurance starts to pay.

WHAT IS CO-INSURANCE?

- Co-Insurance is the amount you are required to pay as your share of the costs of medical services AFTER you pay your premium and deductible.

- Medicare co-insurance is usually 20% of services.

WHAT IS A COPAYMENT?

- A Copayment is the amount you are required to pay for your share of the costs of medical services AFTER you pay your premium and deductible

- Copayments are generally a set cost rather than a percentage.

THE COST OF PART A

Beginning in 2017, in general, these are the costs of inpatient care for those who have Medicare Part A:

- Hospital services: $1,316 for up to 60 days, $329 per day for 61-90 days, and $658 per day for stays beyond 91 days

- Skilled nursing facilities: No charge for the first 20 days, $164.50 per day for 21-100 days, and all costs after 101 days

- Hospice care: No charge for hospice care, $5 copayment for medication, and 5 percent for inpatient respite care (periodic care so your caretaker can rest)

Keep in mind that you have to be admitted to the hospital and approved for these services. Additionally, to qualify for Medicare coverage you have to be in a Medicare-approved facility.

PART B COVERAGE

Medicare Part B covers two things: All preventive services and medically necessary outpatient services.

Medically necessary healthcare includes all the medical care required to diagnose and treat your medical illnesses or conditions, including doctor visits, lab work, medical tests, and medical equipment or devices.

Preventive services refer to the medical services that you receive in order to prevent illness, like a flu shot, or healthcare services undergone for early detection, like routine physicals and cancer screenings.

Additionally, Part B also covers ambulance services, durable medical equipment (DME), outpatient mental health services, second opinions that you need for medical advice, and even a very limited amount of prescription drug coverage.

THINGS PART B DOESN’T COVER

Again, Part B will not cover all the services you may require. The important part to remember is that any care you receive must be considered “medically necessary.” You should always confirm your coverage before having any tests, services, or procedures performed.

It is important to note that the outpatient services that are covered by Part B, require you to meet your deductible and pay any co-insurance or co-payments required.

THE COST OF PART B

You will have to pay a premium for PART B. This is what you can expect to pay in premiums:

| If your yearly income in 2017 (for what you pay in 2019) was | You pay each month (in 2019) | ||

| File individual tax return | File joint tax return | File married & separate tax return | |

| $85,000 or less | $170,000 or less | $85,000 or less | $135.50 |

| above $85,000 up to $107,000 | above $170,000 up to $214,000 | Not applicable | $189.60 |

| above $107,000 up to $133,500 | above $214,000 up to $267,000 | Not applicable | $270.90 |

| above $133,500 up to $160,000 | above $267,000 up to $320,000 | Not applicable | $352.20 |

| above $160,000 and less than $500,000 | above $320,000 and less than $750,000 | above $85,000 and less than $415,000 | $433.40 |

| $500,000 or above | $750,000 and above | $415,000 and above | $460.50 |

The deductible and coinsurance associated with Part B are as follows:

- You pay $185 per year in 2019 for your Part B deductible.

- After you pay the deductible, you will typically pay 20% of the Medicare-approved amount for these:

– Outpatient therapy

– Durable medical equipment (DME)

Also, keep in mind that neither Part A nor Part B gives you prescription drug coverage, so if you are going to opt to enroll in Original Medicare you will also need to pay a premium for Part D coverage or pay for your prescription drugs out-of-pocket. We will cover the coverages and costs associated with part D later in this article.

That should give you a good summary of what is and is not covered in under Original Medicare.

WHAT IS COVERED AND NOT COVERED UNDER

MEDICARE ADVANTAGE (PART C AND USUALLY PART D)?

PART C COVERAGE (MEDICARE ADVANTAGE)

Part C simply refers to Medicare Advantage Plans. These plans cover both Parts A and B of the Medicare program—meaning they provide coverage for both inpatient and outpatient care—and are required to do so by law.

As we will explain in just a moment, Part C plans often have less expensive premiums but they also vary from plan to plan. The premiums are able to be lowered because Medicare Advantage plans have restrictions and limitations about where you can receive your medical care and some plans have limitations on the type of illnesses covered as well.

Remember that Part C plans are run by private insurance companies that contract with the federal government to provide the healthcare coverage. Most Part C plans will also include Part D, or prescription drug coverage, as part of their Medicare package. Some Part C plans even offer basic dental and vision coverage. You can shop around for a policy that has the benefits you want.

THINGS PART C DOESN’T COVER

By law, Medicare Part C plans must cover all the same things as Medicare Part A and B.

But as opposed to Original Medicare, they do cover some services that Original Medicare does not pay for.

For example, most Part C plans include a prescription drug benefit. Another example might be that some Part C plans include eye exams, a pair of eyeglasses each year, or a hearing exam. These difference will vary from plan to plan so please evaluate your needs as you determine the policy you want.

However, Part C will not cover medical services outside your service area. Generally, these plans require you to use specific providers. These are the doctors, hospitals, drug stores and other healthcare providers that the Medicare Advantage plans have contracts with. These are called in-network providers.

It’s important to know that if you use providers outside your plan’s network, it may cost you more money. In certain cases, it may also mean that you the carrier won’t provide any Medicare coverage at all for that service.

Also, be aware that each Part C plan has different rules for how you get services like whether you need a referral to see a specialist, etc. so make sure you understand these rules so that your procedures and services are covered.

THE COST OF PART C

Just like with Original Medicare, you are required to pay a premium for Part C coverage. Because these plans are offered by private insurance companies, we cannot give you the exact amount of your expected premium, but the following may be helpful as you estimate your costs:

- In 2019, the estimated average monthly Medicare Advantage plan (Part C) premium is $28

- Premiums can anywhere from $0 to over $200.

Additionally, just like with Original Medicare you will pay an annual deductible for your healthcare services, in addition to the standard Part B deductible. Some plans that include prescription drug coverage may charge another deductible for drug coverage.

Instead of having to pay a co-insurance percentage, most Part C plans charge a copayment which is a flat fee for services and remember that some types of plans charge higher copays to see providers out of your network.

Each year plans establish the amounts they charge for premiums, deductibles and services.

For your information and estimating purposes, the maximum out-of-pocket spending limit is $6,700 in 2019 for all Medicare beneficiaries, though if you use out-of-network providers, that limit may be higher. Also, some Part C plans offer an out-of-pocket limit below the $6,700 maximum.

PART D COVERAGE

As you already know, Part D covers prescription drugs for Medicare recipients. Part D plans are not offered through the federal government, but only available through private insurance parties.

Individuals can join a standalone Part D Plan or Prescription Drug Plan (PDP) if they have chosen Original Medicare or they can sign up for a Medicare Advantage Plan (Part C) in which Part D is included. You cannot opt to enroll in Part D alone. You are only eligible to add Part D coverage if you have signed up for benefits under Parts A or B.

Each insurance company will provide a list of approved prescription drugs which are covered under their particular plan. So, when you choose your plan it is important to know what your prescription needs are and cross reference that list with the available Part D options, making sure your policy covers the medicine you need.

THINGS PART D DOESN’T COVER

Part D only covers a certain number of drugs. Every day new drugs are researched, developed, and manufactured and it takes time for these new drugs to appear on the Part D coverage lists.

Part D does not cover experimental drugs.

COSTS OF PART D

Just like Part C plans, Part D plans vary in cost from plan to plan and from carrier to carrier. However, the following information may help you understand and estimate your costs of having a Part D plan.

- The average monthly Part D premium in 2019 is $33.19, although premiums vary depending on the plan you choose and where you live.

- You will generally only want to choose a plan with low premiums if it also has the lowest overall cost per year, including the costs for the drugs you take.

In addition to a premium, many plans require a separate prescription drug deductible. Remember these kinds of policies will not pay for your prescriptions until you pay the deductible amount out-of-pocket.

- The maximum deductible a plan can charge in 2019 is $415.

- There are plans that have $0 deductible or ones with lower maximums like $150 or $250.

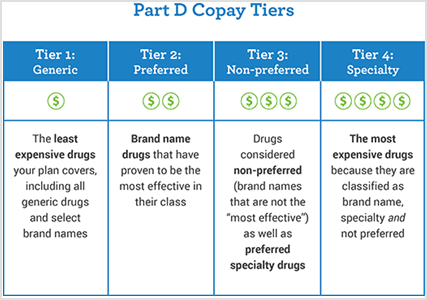

Prescription drugs are arranged in tiers. Premiums and copayments can change depending on which tier of medicine you need.

Prescription drugs are arranged in tiers. Premiums and copayments can change depending on which tier of medicine you need.

When you need a top-tier drug, which is often a new or very expensive, it can increase your premium, copayment, or coinsurance.

Just like your other healthcare coverage, you will have the cost of a copayment or coinsurance with your prescriptions. Remember that a copay is a fixed dollar amount for your prescriptions.

For example, you might have to pay $5 for a generic drug, $40 for a “preferred” brand name drug and $75 for a non-preferred brand name drug.

Coinsurance is a percentage of the price of your prescription. Typically plans require coinsurance for drugs listed in higher tiers like tier 4 and tier 5 drugs. For example, if your prescription costs $400, and your coinsurance is 25%, you will pay $100.

Note that it is possible that some of your medications require a fixed copayment and others a coinsurance.

At this point, you should have a very good understanding of what is covered and not covered under each part of the Medicare program and the costs associated with each.

HOW DO I FIND THE BEST MEDICARE COVERAGE FOR ME?

Even with this thorough breakdown of what is covered and not covered by Medicare, it can be overwhelming as you consider your choices.

How will you decide what is best? Luckily you do not have to do it alone. Many people are ready and able to help you navigate the Medicare options that are available for you, including licensed and experience Medicare insurance agents

At Insurance Professional of Arizona, we have an engaged team of brokers that are experts in Medicare insurance. Together we have decades of expertise and knowledge to help answer your questions and help you find the right plan for you.

Does it make more sense to choose Part A, B, and D? Or would you be better off with Part C and the extra coverages that come with it? Are you more concerned about your premiums and costs or more concerned about getting care wherever you are?

Are you willing to pay the coinsurance that accompanies Original Medicare or would it better to include a Medicare supplement plan to help offset those out-of-pocket costs? We can help you assess your personal needs and answer these questions so that you end up with the right Medicare plan for you.

At IPA we not only want to make sure you have the right plan with the right amount of coverage, we always ensure that our clients have the best coverage at the most affordable and reasonable prices. Being independent agents means that we can shop lots of competing health insurance companies to get the most competitive policies with the extra benefits you need and deserve.

FINAL WORDS!

Please contact our office for help in setting up your Medicare plan.

Please contact our office for help in setting up your Medicare plan.

We will walk you, step-by-step, through the enrollment process after thoroughly evaluating your personal needs, so that you have the benefits you need without ever paying any penalties or getting stuck without coverage.

To get started today, just call us or fill out the contact form right here on our website. At IPA, our experienced and professional Medicare agents will help you successfully navigate the Medicare program and get the health insurance policy that’s right for you!

We’re here to help! Call us today.

Share your thoughts

Leave your comments